- UK productivity growth has been chronically low for years

- The large public sector is the source of the problem

- If so, will the government do anything about it?

Yesterday I mentioned Bank of England Governor Andrew Bailey.

And that he appears to have been reading Fortune & Freedom.

In comments last week he suggested that high public sector employment growth may be to blame for the UK’s historically low productivity growth.

Let’s look at exactly what he said.

As reported in The Telegraph:

Andrew Bailey has warned that Britain’s bloated public sector is dragging down the economy after the Bank of England slashed its 2025 growth forecasts in half.

The Governor of the Bank of England said an increase of half a million workers in the public sector since lockdown had not been matched by a rise in productivity.

Speaking after the Bank slashed growth forecasts for 2025 from 1.5pc to 0.75pc, Mr Bailey said: “It is fair to say we have seen an increase in public sector employment. We haven’t seen a commensurate increase in measured public sector output.”

The Bank blamed an “increasing share of employment accounted for by areas where the public sector is the predominant employer such as education, health and public administration” for holding back productivity growth in the past few years.

It added: “Employment in these areas has risen significantly since 2019, particularly in health-related activities, but these sectors have also seen significant declines in their measured productivity per hour. This means that the shift in the composition of total employment towards these areas will have weighed on total productivity.”

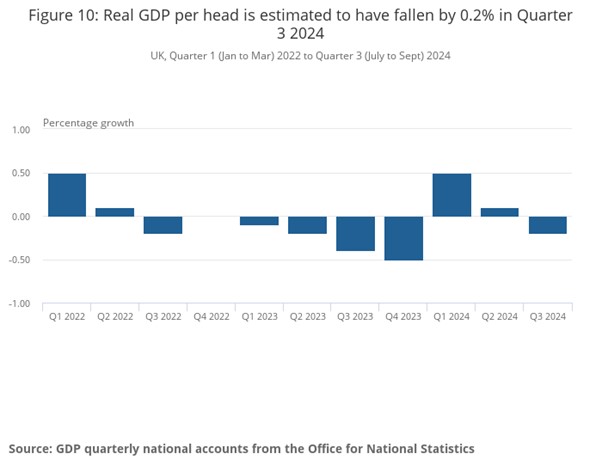

Indeed, the economy has grown, if only very slowly, in recent years.

But when adjusted for population growth, output has shrunk. This can only be explained by outright negative productivity growth.

Here is a chart of GDP per-capita from the Office for National Statistics (ONS):

This is exactly what we wrote about in an article back in August 2023. Here is a relevant excerpt:

[T]he UK has been slipping in relative, per-capita prosperity terms versus the rest of the developed world. A recent report by the Organisation for Economic Co-operation and Development (OECD), which is comprised of 38 of the world’s wealthiest countries, shows that the UK has slipped into the bottom half of its members for the first time.

The UK is thus underperforming as an economy both relative to its own history and the rest of the world, and these trends have been in place for many years, if not yet a full generation.

This begs the question of why? What is it about the UK that is resulting in economic stagnation and relative underperformance?

Here was our suggested explanation at the time:

It comes down to the so-called “productivity puzzle”, that is, that the UK has been going through a prolonged period of low – indeed near zero – productivity growth.

None of the above paints a pretty picture: the UK is a high-tax, highly regulated, over-financialised economy that increasingly concentrates income and wealth at the top, rather than one which provides prosperity for all.

And we had this to say earlier this month:

When resources get constrained in a relatively low-growth place, that’s when you get stagnation.

Sometimes governments stand in the way. They protect jobs in declining industries, impeding the flow of workers and capital to newer, faster-growing ones.

The lowest growth place of all is government itself. Oh, sure it can grow, but only by appropriating private sector resources via taxation.

If Britain wants to get growing again, it needs to allow resources to flow to where they are most productive and profitable. It needs to shrink the size of the state.

“Round up the usual suspects!”

Mr Bailey has thus correctly identified the culprit behind the productivity puzzle. And none too soon, given that Britain’s relative economic underperformance has already lasted nearly a full generation.

But will the government even notice? Or will it “round up the usual suspects” instead and keep blaming capitalism and profit-seeking businesses for Britain’s economic woes?

If the government truly wants to go for growth, it needs to solve the productivity puzzle. It needs to stop growing the public sector at the expense of the private.

If you’re sceptical the government will come round anytime soon, should you invest in Britain? Perhaps you should internationalise your wealth and invest abroad instead. Fortunately, this is as easily done as said.

The UK is home to a large number of multi-national, world-class companies. Did you know that over 80% of FTSE 100 constituent company revenues are sourced from overseas?

Some of those companies are more international still, with 95%+ of revenues coming from elsewhere. So, while one might despair at the state of things in the UK, British investors have easy access to investments on friendlier shores.

Here at Southbank Investment Research, we provide our members with practical, actionable ideas to take full advantage.

However if you’re still looking to invest British, my colleague James has something up his sleeve.

Until next time,

John Butler

Investment Director, Fortune & Freedom

Off the Wall

Bill Bonner, writing from Baltimore, Maryland

‘I object, your honor! This trial is a travesty. It’s a travesty of a mockery of a sham of a mockery of a travesty of two mockeries of a sham.’

– Woody Allen, in ‘Bananas’

NPR (last November):

A duct-taped banana sells for $6.2 million at an art auction

A piece of conceptual art consisting of a simple banana, duct-taped to a wall, sold for $6.2 million at an auction in New York on Wednesday, with the winning bid coming from a prominent cryptocurrency entrepreneur. At one point, another artist took the banana off the wall and ate it.

What follows is a reverie about price, value… and bananas.

Guess how much stocks have gone up over the last 100 years… how much more valuable are they than they were in 1925?

Go ahead. Take a guess.

The answer, according to our new Law of Conservation of Value is… zero.

Since this seems to contradict the evidence (below) and almost everything we think we know about the stock market and the nature of American capitalism, an explanation is in order. But in order to understand it, we need to put on our life preservers as well as our thinking caps… and jump into a sea of slippery numbers.

First, there are lots of different kinds of value. A banana at an art auction may be worth $6.2 million. In the grocery store they sell for 60 cents a pound. What is Bitcoin worth? How about a baseball card?

Things have value inasmuch as people value them. The $Trump coin, for example, is worth something… but only because people want to own it. You can’t eat it. You can’t use it to shovel snow. Maybe it will increase in value… or maybe it won’t.

Most things get their value based on what they do for you. Cars transport you. Houses protect you. But there is also a big aesthetic… or perhaps vanity… component. People want to buy stylish clothes… live in nice neighborhoods… or drive fancy cars that enhance their feeling of well-being, even if they don’t really provide any extra utility.

We are a competitive species… always looking for ways to show off. Often, we pay for it. When people buy bananas at the grocery store, they may try to get the most for their money. But when they buy bananas duct-taped to a wall, they are trying to get the least value for their money. Spending recklessly is proof that they are rich… and perhaps ‘above it all.’ That’s why people buy Gucci handbags or Rolex watches, too. There is little extra utility, but the extra expense sends a message.

Even in the financial world, many people buy things that seem like preposterous places to put money. They buy a crypto or a ‘meme’ stock and claim to be ‘investing.’ What they are really doing is betting that someone will be an even ‘greater fool’ and pay more.

But let us set aside the imponderable world of gambling and vanity spending. Let’s look instead at real world output – the goods and services that most of us want and need – and the capital values of the businesses that produce them.

Ford produces autos and trucks. Its value comes off the assembly line. Today, it makes more and better vehicles than it did a century ago; does that make it more valuable?

Oil companies pump more oil, too. Movies are more sophisticated… and home heating, generally, works better. Progress!

Do these improvements increase the value of Ford or other companies? Not necessarily. Values are relative, not absolute. When everyone gets absolutely richer, no one really gets relatively richer. And just because Ford produces more and better cars doesn’t necessarily mean it is worth more… compared to other things.

So, in order for stocks (or anything) to be worth more… they must be worth more in relation to other items of value. And other things are making Progress! too.

The role of money is to make it easier to figure out. If you grow a crop of tomatoes, and you want to exchange it for other things you want or need, your crop will turn to mush before you get very far. Is a newspaper subscription worth 30 tomatoes… or 25? Is a pair of shoes worth 200? But what shoemaker wants 200 tomatoes?

Money also made it possible to establish a ‘price.’ People who want tomatoes can bid against each other. Each has his own wants, needs, and information. The ‘market’ takes it all in, aggregates it, and distills it into a single number… a market price.

In dollar terms, over the last 100 years, cars have gone up about 83 times. Houses are 85 times more expensive. But stocks? They’re up 366 times since 1925. Nothing else comes close. (More detail tomorrow…)

But how could the makers of ‘stuff’ be so much more valuable than the ‘stuff’ they make?

Have the markets gone bananas?

Regards,

![]()

Bill Bonner

Contributing Editor, Fortune & Freedom

For more from Bill Bonner, visit www.bonnerprivateresearch.com