Somewhere in Shenzhen, inside a heavily secured facility, a team of engineers working under fake identities has been trying to reverse-engineer one of the most complex machines ever built.

Somewhere in Shenzhen, inside a heavily secured facility, a team of engineers working under fake identities has been trying to reverse-engineer one of the most complex machines ever built.

The machine is an extreme ultraviolet lithography (EUV) scanner, made exclusively by a single Dutch company called ASML [Nasdaq: ASML].

It weighs 180 tonnes, requires 41 trucks to transport, and contains over 100,000 individual components. Each machine costs around $500 million — and without it, you cannot manufacture the advanced memory chips that are the lifeblood of AI.

The espionage campaign has been running for years.

Former ASML engineers were recruited, some given aliases to conceal their involvement.

Over two million lines of proprietary control software were stolen by employees at a startup called XTAL, whose leadership fled to China. A US court even awarded ASML US$845 million in damages. A separate employee was linked to a Beijing-backed intelligence ring.

Late last year, reports emerged that a covert Chinese lab had assembled a prototype EUV system, attempting to replicate ASML’s laser-produced plasma method from scratch.

The only problem: they’re not even close.

Despite years of effort, they still cannot crack the code. Most estimates suggest they remain roughly a decade behind.

And that’s what makes this so remarkable.

It’s not the espionage. Not the stolen code, the false identities, or the secret labs.

It’s that these machines have become some of the most valuable assets on earth and without a handful of the world’s rarest metals, none of this exists.

The biggest equipment order in chipmaking history

This week, SK Hynix, one of the world’s leading memory producers placed an $8 billion order with ASML for EUV scanners, the largest publicly disclosed equipment deal in semiconductor history.

These machines will be deployed across fabrication plants in Cheongju and the new Yongin Semiconductor Cluster in South Korea, producing high-bandwidth memory (HBM) and advanced DRAM (short-term working memory) for AI systems.

At the same time, SK Hynix confidentially filed with the SEC for a US listing that could raise up to US$14 billion, with funds earmarked for more chip factories in South Korea and Indiana.

For those unfamiliar, SK Hynix is the world’s dominant supplier of HBM, the memory chips inside Nvidia’s AI accelerators. It controls more than 60% of the global HBM market and is Nvidia’s primary memory partner.

A US listing aims to close a valuation gap with Micron [Nasdaq: MU] while raising the capital needed to keep building and trying to supply a market that has insatiable demand for memory.

In total, that’s more than $20 billion being deployed to secure access to some of the most advanced — and tightly controlled — technology on earth.

And every dollar points back to a constraint we’ve been highlighting: there simply isn’t enough supply of the physical materials required to build what AI demands.

That spells good news for the companies trying to dig it all up to meet that demand.

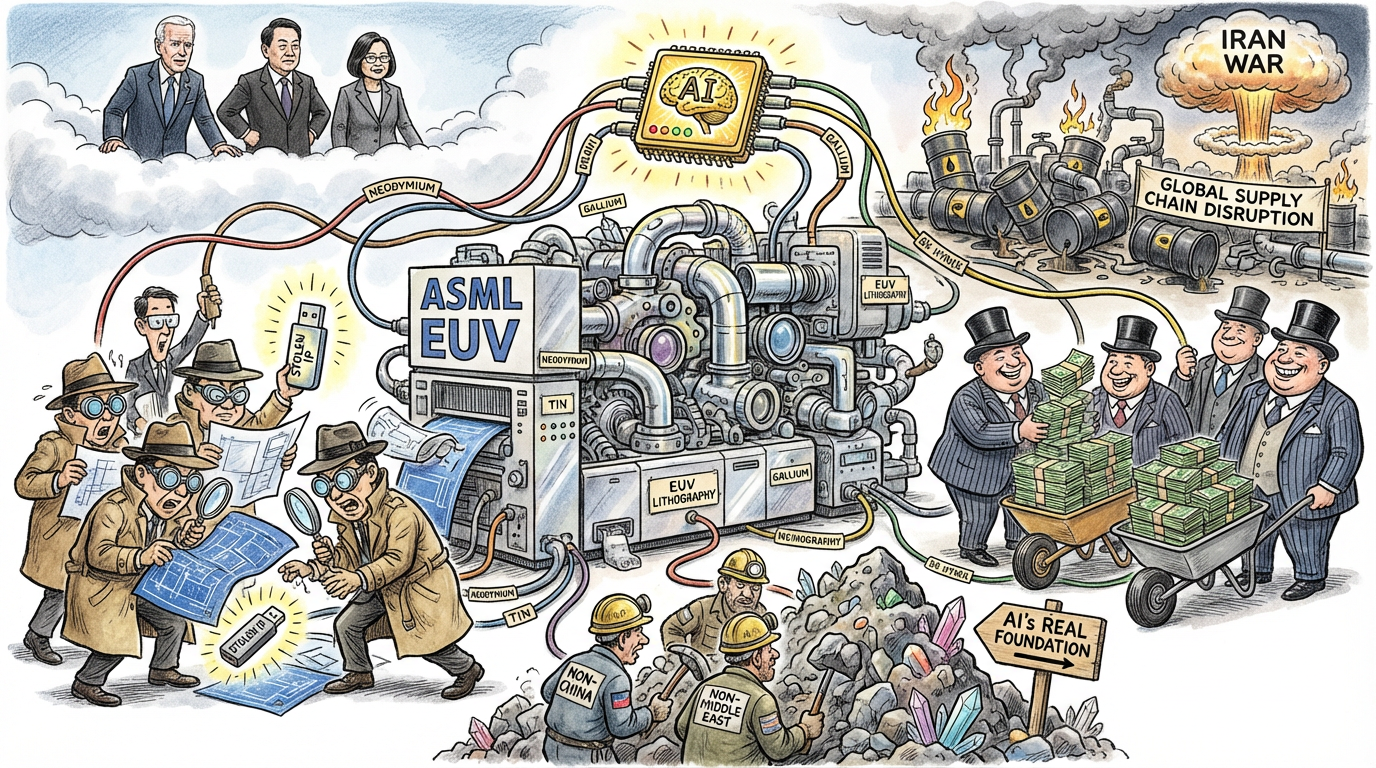

Every EUV machine is a shopping list of metals you’ve never heard of

Each of the machines SK Hynix just ordered a complex chain of critical materials. Neodymium for high-precision magnets. Molybdenum and silicon for ultra-thin mirror coatings. Tin for the plasma light source. Yttrium and gadolinium for optical coatings. Cerium oxide for wafer polishing. Gallium and germanium for compound semiconductor substrates.

And that’s before you count the rare-earth inputs needed for the memory chips produced inside them.

China controls around 70% of global rare earth production and around 90% of global rare earth processing.

To say there’s a genuine concern globally of this tight supply chain is an understatement.

If the US wants to dominate AI manufacturing and infrastructure, it desperately needs the technology from the likes of SK Hynix, Micron, Nvidia, etc. Those companies, in turn, desperately need the technology from companies like ASML and Taiwan Semiconductor (TSM)… and they all desperately need the critical metals to make it happen.

Just one slight problem at the moment…

They’re all stuck because of the war in Iran.

Taiwan and South Korea, where the vast majority of advanced memory is made, are almost entirely reliant on imported energy. Taiwan sources around 95% of its crude from the Middle East.

When oil prices spike, the cost of running fabs rises in lockstep, and so does every upstream process like mining, refining, smelting, and transporting the critical metals that go into the machines and the chips.

We already had a memory shortage. We already had constrained supply of critical metals under Chinese export controls. Now there’s an energy shock layered on top.

So, who do you think really wins from all this?

For me, the logic is clear.

AI needs chips.

Chips need memory.

Memory needs EUV machines.

EUV machines (and everything else) need critical metals.

Critical metals need energy to mine, refine, and ship.

And energy is in its most disrupted supply shock in history.

That means the real opportunity may lie with the companies supplying those inputs — particularly those operating outside China and the Middle East.

They are the foundation beneath the foundations.

Without them, the EUV machines don’t get built. Without the EUV machines, the memory doesn’t get made. Without the memory, AI doesn’t scale… and the US fails to deliver on a very big and expensive promise.

Nations are deploying spies to steal the blueprints. Companies are spending US$22 billion in a single week. But what it all comes down to is rocks in the ground.

And rocks in the ground is something that Matt Badialli, editor of Real Wealth Insider, is an expert in. He’s a trained geologist. He’s been CEO of a mining company. He’s been walking mining properties and finding the best investments in resources for decades.

Now, he’s pinpointed the next 9 investment plays that are building momentum.

Until next time,

Sam Volkering

Investment Director, Southbank Investment Research

PS Billions are being spent on AI infrastructure right now.

But as you’ve just seen, the real bottleneck isn’t technology — it’s resources.

That’s exactly where the next big move is forming. And most investors haven’t caught on yet.