Yesterday, OpenAI closed the largest private funding round in history.

$122 billion raised.

$852 billion valuation.

Amazon, Nvidia, SoftBank, and Microsoft all coughed up the big bucks for it.

And, for the first time, individual investors were able to participate, pouring in $3 billion, albeit through what OpenAI described as “bank channels.”

OpenAI said the round exceeded the size of the largest IPO ever completed – and the company isn’t even public yet.

But that highlights the key point.

This may have been the last time OpenAI raises capital privately.

Anthropic and SpaceX are racing toward public listings. Combined, their private valuations sit around $2 trillion, with SpaceX accounting for the majority.

Add in an OpenAI IPO in the second half of 2026, and we’ll all have a front row seat to the single most consequential year for IPOs in history.

All this with the backdrop of all that in the US and Middle East…

If you are prepared for these mega IPOs, the opportunity extends beyond short-term gains. This could represent a multi-year wealth creation cycle not seen since the period following the dot-com bust.

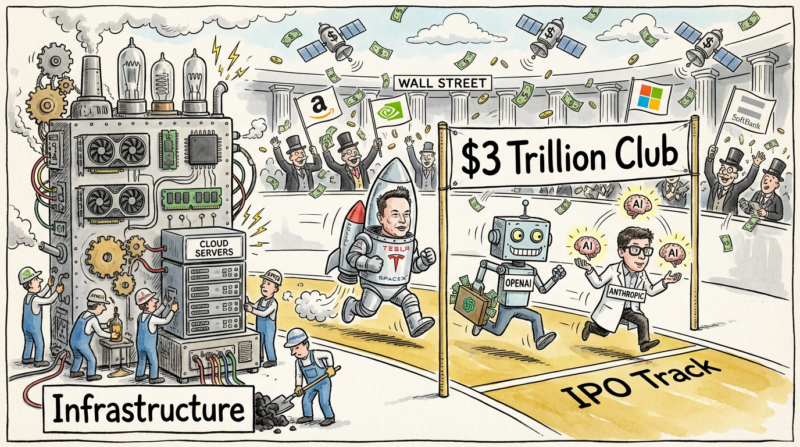

The race is on

SpaceX is closest to launch. It could file as early as this week.

Morgan Stanley and Goldman Sachs are leading the underwriting. The target is a $75 billion raise at a valuation between $1.5 trillion and $1.75 trillion.

If achieved, it will be the largest IPO in history, eclipsing Saudi Aramco’s $29 billion listing in 2019 by an almost comical margin. It would also make OpenAI’s recent valuation appear relatively modest by comparison.

Why does that matter?

Because Elon Musk and Sam Altman are competing head-to-head, and that rivalry is likely to drive bigger, faster moves on both sides.

At this stage, Musk appears to be ahead.

The SpaceX IPO is so big that the Nasdaq just adjusted its rules to accommodate it. From May 1, mega-cap IPOs can join the Nasdaq 100 index within 15 trading days of listing, down from roughly three months. That means every passive fund tracking the index has to buy.

Once that is complete, Anthropic is expected to follow. It recently closed a $30 billion funding round and may IPO as early as October, with Goldman Sachs, JPMorgan, and Morgan Stanley in early discussions.

There is also speculation that the eventual raise could exceed $60 billion, potentially making it the second-largest IPO in history.

OpenAI will likely follow. The recent $122 billion round was almost certainly its final private raise, with an IPO expected before the end of the year.

Maybe it also comes sooner. There’s a legitimate worry that if Anthropic lists first, it could absorb a massive build up of retail demand for pure AI exposure.

Each company wants to list — but more importantly, each wants to be the largest.

Attention here, opportunity over there

However, by the time these companies list, much of the upside may already be priced in.

Private funding rounds have already priced in years of growth. A SpaceX IPO at $1.75 trillion or OpenAI near $1 trillion implies valuations comparable to the world’s largest public companies before trading even begins.

For substantial returns, valuations in the tens-of-trillions need to come.

That might be hard.

So where’s the real opportunity?

It lies in the infrastructure these companies depend on. And it’s the exact segment of the market that’s been hammered in the last few weeks.

OpenAI is very clear about what it needs.

It relies on GPUs from Nvidia GPUs, AMD chips, AWS Trainium, Cerebras processors, and a custom chip built with Broadcom. On the cloud side, it depends on Microsoft Azure, Oracle, AWS, CoreWeave, and Google Cloud.

And behind those companies sits another layer – fabrication, critical metals, memory, and the emerging “neocloud” providers scaling to meet demand.

Nvidia just inked a deal with Nebius for exactly this reason.

Anthropic is on a similar path, committing up to $50 billion to US infrastructure.

SpaceX, meanwhile, envisions up to a million satellites acting as orbital compute nodes, powered by continuous solar energy and cooled naturally in the vacuum of space.

That requires advanced semiconductors, memory, power systems, optical networking, and critical materials at a scale that doesn’t yet exist.

Whatever you are hearing about demand collapsing may hold in the short term. In the long term, the scale of this build-out is too large to ignore.

Memory makers like Micron, SK Hynix, and Samsung are still sold out years in advance. Nvidia is deepening its lock on AI training and inference. AMD and Broadcom are carving out critical roles in custom silicon. Cerebras is emerging as a real alternative for inference workloads.

When hundreds of billions in IPO capital enters public markets at multi-trillion valuations, the entire semiconductor, memory, networking, and materials supply chain stands to benefit.

For long-term investors, recent pullbacks may represent opportunities to build positions at more attractive levels.

Earlier this year, I wrote that 2026 would be the year of shortage before excess. Now we know exactly where the capital is flowing, and exactly who needs what to keep the engines running.

The IPO race is on. But it’s still the infrastructure trade as the way to play it.

Until next time,

Sam Volkering

Investment Director, Southbank Investment Research

PS IPO headlines might grab the attention.

But right now, there’s a much bigger force shaping markets: geopolitical tension, shifting rates, and capital moving beneath the surface.

And historically, it’s not the moment everyone is watching that creates the biggest opportunity, as I just pointed out…

It’s what comes just after.