In today’s Issue:

In today’s Issue:

- How to hunt for ten-bagger stocks

- Mining and AI are just one match made in heaven

- The company that’ll revolutionise AI and clean your bum

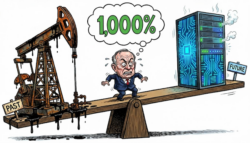

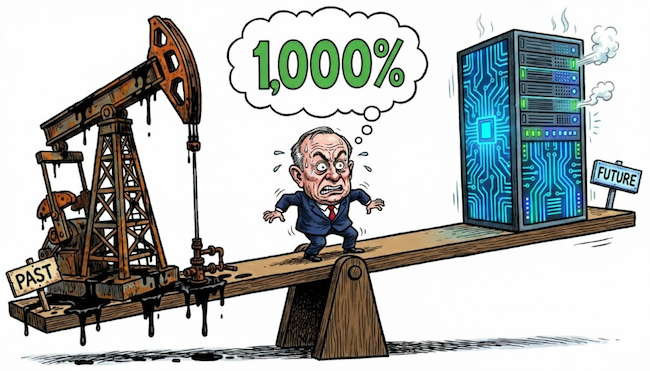

Ten-baggers are rare. Stocks don’t go up 1000% without a reason. It takes something special.

Even rarer is when an entire industry goes bananas, creating a whole flock of ten-baggers for investors from the same sector.

And it’s almost unheard of for an established industry full of sizable companies with long operating histories to do just that.

I can only think of one example: the US shale oil and gas boom.

Fracking unleashed one of the most economically and geopolitically important developments of the last 50 years. The combination reshaped the US economy, global oil and gas markets, and redefined geopolitics.

Fracking turned the US from a major energy importer into the world’s largest oil and gas producer. The US also became the world’s largest exporter of LNG.

The shift helped reign in the US trade balance and propped up the petrodollar link between energy and US dollar trade.

It smashed the OPEC cartel’s control over oil markets and thereby geopolitics.

It allowed the US to dodge Europe’s deindustrialisation by keeping domestic energy prices far lower.

That energy fuelled the US AI data centre boom while much of the rest of the world lagged behind.

It pushed US GDP growth far ahead of other developed economies.

It delivered cheaper energy to US consumers — an estimated $800 billion per year in savings, roughly 3% of GDP.

It shifted a large chunk of global LNG trade onto the oceans, making supply sourcing more flexible and competitive.

In Pennsylvania alone, the natural gas industry generated over $5.8 billion in local, state, and federal tax revenues in 2022.

It also delivered a long list of ten-bagger stocks. In many cases they were established oil and gas companies.

What makes a ten-bagger possible?

The real paradox is that America had known about its four key oil and gas basins for decades — just as Britain knows about its own today. But much of that shale wasn’t economically recoverable.

Modern fracking innovation is what turned those resources into reserves, meaning they became economically viable to extract. It also made existing wells dramatically more profitable. The boom was on.

Fracking turned marginal shale oil and gas into a $1.4 trillion sector.

No wonder stocks soared by thousands of percent…

But here’s what I want you to focus on: fracking made oil and gas more productive. It radically increased production from the same wells.

In this month’s issue of The Fleet Street Letter, we explored how to profit from the next big fracking boom.

But oil and gas is hardly the only industry to undergo a radical revolution thanks to a spike in productivity.

Mining and AI are a match made in investors’ heaven

Just as fracking revolutionised the shale oil and gas industry, Artificial Intelligence is upending the mining. It is making mines radically more efficient. It is crushing mining costs, and it is revealing hidden ore bodies with its vast analytical power.

Just as fracking made run-of-the-mill shale oil and gas stocks dramatically more valuable, AI will for mining companies.

Combined with President’s Trump’s push to accelerate mine permitting, another extraordinary boom could be brewing in one particular sector of the stock market.

Here’s our favourite way to profit from AI’s impact on mining.

But here’s the irony…

AI itself needs the same productivity revolution

The CEO of Aussie company Goodman Group (GMG.AX) has been trying to explain to his shareholders that demand for AI data centres far exceeds supply.

And so the company’s extraordinary pipeline of AI data centre construction projects is a home run, not a risk.

He may be right about the demand. But what about supply?

The AI data centre industry is already coming up against a lot of constraints.

Energy, infrastructure, organised labour, and government regulation all threaten to slow the boom — much as environmental opposition kneecapped fracking in parts of the UK and Europe.

Capital investment into AI will have to solve a lot of problems if it wants to continue data centre expansion.

Capital flowing into AI will have to solve a long list of problems if data centre expansion is to continue.

Power grids must be upgraded. Power plants built. Communities reassured that robots won’t take their jobs and bribe a lot of politicians.

The question is how to pull all this off.

There are two paths.

The first is the “more” strategy.

The AI boom could produce more of its own electricity and infrastructure to carry its own burdens.

It could build more data centres to add computational power.

It could construct more infrastructure to move more data.

If you want to bet on the “more” strategy, there are plenty of fantastic investments. Stocks like Goodman Group, for example.

Atlas Energy Solutions (AESI) is pivoting from providing sand to fracking companies to building power plants for AI data centres.

But I think the second strategy is the more promising one.

More with less

Imagine fracking hadn’t revolutionised shale oil and gas production. The US would’ve needed an astonishing amount of oil and gas wells to meet its record breaking production today.

It probably would never have drilled those wells. Shale oil and gas only produce a small amount per well without fracking. They wouldn’t have been profitable competing with low-cost producers from around the world. Leaving the US as a major energy importer instead of net exporter.

A “more” strategy wouldn’t have worked. And it certainly wouldn’t have delivered ten-baggers.

Instead, fracking made each well dramatically more productive. It enhanced the existing stock’s capacity and made the companies which owned that stock dramatically more valuable.

Of course, this did end up allowing more wells to be drilled. But fracking’s effect was all about achieving better results from the same well.

Efficiency gains can actually spike demand for a product by making it cheaper per unit of output. We use more oil and gas when producing them gets cheaper.

The same applies to AI. Its uses will only expand if it gets more efficient. The Goodman Group may yet hit a home run.

And that’ll mean this opportunity explodes even further.

But my real point is that the AI boom is entering a phase where efficiency gains may be the key issue at hand.

Why the DeepSeek panic was so visceral

Last year, the AI industry panicked over news China had come up with a more efficient form of AI.

Beyond branding it with a catchy name, DeepSeek claimed to have revolutionised the amount of inputs needed to run AI. It needed less chips using less energy.

The claims unravelled. But they were enough to cause a panic. Because if they had been true, superior efficiency threatened to outcompete American AI.

It was a bit like OPEC’s panic over US fracking. Which makes you wonder who was behind European fracking bans. But that’s another story.

In coming years, modifications to AI that enhance efficiency will prove to be the most valuable investment plays. Just as fracking changed US oil and gas from a struggling industry eeking out profits to a ten-bagger production line.

The “more” strategy will five way to “how to do more with less” at each AI data centre — energy efficiency, compute efficiency and other innovations.

It’ll trigger another long list of ten-baggers amongst the companies that make AI more productive per unit of input.

Some may l be stocks that used to be noticeably boring. A bit like the recent craze around a Japanese toilet company whose ceramics business is used in AI. Don’t ask me how. I have enough trouble operating their toilets. My in-law’s one has 38 buttons!

One company will kick off this AI efficiency craze in just a few days’ time.

Until next time,

![]()

Nick Hubble

Editor at Large, Investor’s Daily

P.S. The AI boom is about to shift from “more chips” to “more efficiency.” This tiny company is already mass-producing the hardware Nvidia needs to make that shift — and the blue spike just flashed. See the full briefing before the market catches on.