Editor’s note: While this essay focuses on U.S. interest rate dynamics, the implications for UK investors are clear. When Mr. Market turns in the U.S., the ripple effects hit the UK bond market, FTSE-listed multinationals, and even the pound. A global debt cycle driven by distorted rates doesn’t stop at Dover.

That’s why we watch Washington as closely as Westminster—and why understanding the mechanics behind interest rate manipulation is essential to protecting (and growing) your wealth on this side of the Atlantic.

Let’s return to the question ‘What to do with your money now?’ keeping in mind that things can change, fast.

On Monday, we were at war. By Tuesday, it was ‘TIME FOR PEACE.’ And now, investors hold their breath, awaiting the next news flash. Trump vs. Powell, the US vs. Iran war, the Big, Beautiful Budget Abomination vs. fiscal rectitude…ICE vs. ‘illegals’…the Supreme Court vs. Presidential power – at any moment, the artillery shells could begin landing.

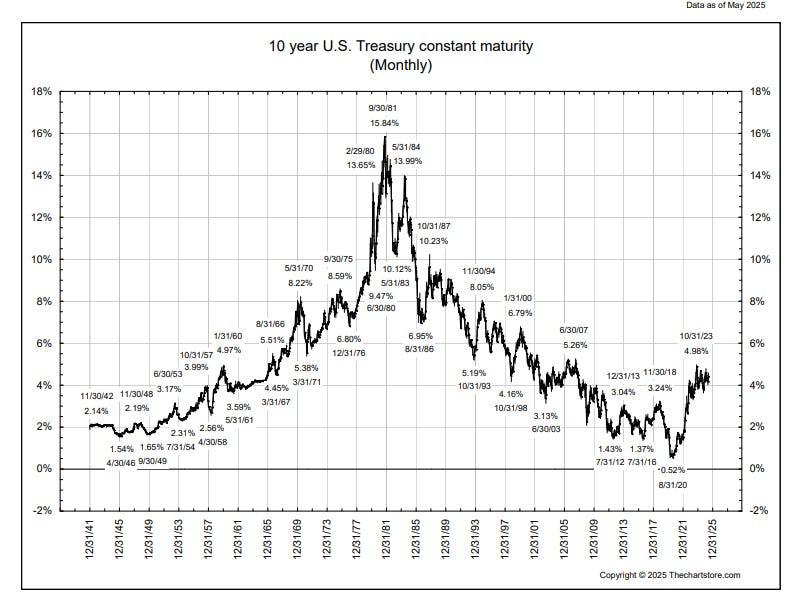

And bonds are an obvious target of opportunity. They appear to have entered a long-term primary downtrend. If the patterns of history repeat themselves, we could be looking at higher interest rates for the rest of our lives.

Interest rate cycles may reflect the human life cycle. Before 2020, the last low for yields came about the time we were born — after WWII. You could get a 4% mortgage in the late ‘40s. And then you had to wait about 70 years to refinance at the same rate.

Mr. Market controls the long cycles in bond yields. But Mr. POTUS thinks he knows better. He wants the Fed to cut rates and keep them low. Trump:

“Europe has had 10 cuts, we have had ZERO. No inflation, great economy – We should be at least two to three points lower. Would save the USA 800 Billion Dollars Per Year, plus. What a difference this would make.”

What difference would it make?

One of the differences came in the news today, Bloomberg:

Dollar Weakens as Trump Considers Naming Next Fed Chair Early

Bloomberg’s gauge of the greenback dropped to the lowest level in three years.

A lower dollar makes differences of its own. Imports become more expensive. Add tariff taxes and price hikes can be substantial, making consumers poorer.

Digressing for a moment, poverty is not always easy to see. Average wages can rise…even as most people have less money and less spending power. GDP can go up even as it becomes harder and harder to find a good job or afford a decent place to live.

Recall that the Biden team had trouble convincing voters that the economy was strong. The statistics said so. But people didn’t believe it.

We’ll come back to this subject — the fakiness of our ‘leading’ statistics — but here’s a hint. Newsweek:

While headline unemployment may be stable, an increasing number of Americans are experiencing what is referred to as “functional unemployment,” a term that highlights the deeper issues facing America’s workforce.

According to the Ludwig Institute for Shared Economic Prosperity (LISEP), 24.3 percent of the country now find themselves “functionally unemployed,” defined as “the jobless plus those seeking, but unable to find, full-time employment and those in poverty-wage jobs.”

Would lower interest rates help? Between 10% and 0% are 1,000 basis points. The odds that POTUS will know exactly which one the economy needs are very, very low. The right rate is not chosen – neither by the Fed or by the president. Instead, it is discovered by Mr. Market.

In practice, politicians always want lower rates. People borrow and spend. Laissez les bons temps rouler…and get re-elected. But interest rates are a price — the price for using someone else’s savings. And like any price, it gives us valuable information about the amount of savings available, the eagerness of borrowers, and so forth. Any interest rate chosen by anyone other than Mr. Market himself is likely to be ‘wrong.’ It will convey false information to both borrowers and lenders.

Don’t lower rates encourage employment and GDP growth? Maybe. But only if they are true. Following the mortgage finance crisis, the US had more than a decade with the lowest interest rates in history. Below zero, in real terms, for much of the period. But the only thing that changed substantially was the level of US debt. It toted to $10 trillion in 2008. By 2020, it was up to $27 trillion.

Lower interest rates encourage borrowing. That’s the whole idea. Debt goes up. Spending goes up. The feds ‘print’ more money to cover their deficits. Prices rise further.

Then, interest rates go up, as lenders anticipate more inflation…and sooner or later bonds go down as the full faith and credit of the US government erodes.

There’s nothing new about this. Nothing we don’t know already. The cycle is unrelenting. Uncompromising. Irresistible. Logically inevitable. Empirically proven.

Bonds rise. Then, they fall. The politicians can blab and bluster. Fed governors can pretend to know what they are doing. But Mr. Market always has the last word.

Regards,

![]()

Bill Bonner

Contributing Editor, Investor’s Daily