In today’s issue:

- Many economic statistics are subject to large revisions

- Last week the US economy “lost” some 600k jobs

- What are investors to do, if economic data are unreliable?

Data is messy. It may reduce to numbers, but even those are subject to measurement error and hidden assumptions. “Why those numbers, and not others?” one should always ask.

Bad data leads to bad conclusions. Every time.

This is particularly the case when it comes to human affairs. Reducing the collective actions and reactions of conscious, thinking – if often irrational – beings to raw numbers is, at best, a rough approximation of what is really going on.

At worst it’s outright misleading and, if used to inform economic policy, can do much harm. Economist Milton Friedman won the Nobel Prize in Economics in part due to his work asserting that the US Federal Reserve was not only partly responsible for causing the Great Depression, but for prolonging it too.

Friedrich von Hayek also won the Nobel Prize in Economics for his work on so-called Austrian business cycle theory. In his Nobel memorial lecture he warned economists and policymakers more generally against the “pretence of knowledge” or “fatal conceit” implicit in the central planning of human affairs.

“First do no harm” goes the classical Hippocratic Oath of medical practice. But it is equally applicable to economic or social policy.

In the most recent, prominent example of economic data being wildly off the mark, last week the US Bureau of Labor Statistics revised away some 600,000 jobs.

That’s right. 600,000 jobs that supposedly existed, but actually don’t.

The US workforce is some 160 million. So, we’re talking about a revision of only 0.4%. But if you’re one of those 600,000 who supposedly had a job, you’re probably out looking for one instead.

In other words, the US economy is weaker than previously estimated, if only by some 0.4% of the previously-assumed workforce.

That might not seem important, but it is.

The global economy has been weak over the past year. There are, as yet, no signs that it’s strengthening. If anything, leading indicators point to an ongoing stagnation.

If the data is to be believed, the US has been a relative bright spot. Perhaps not as bright as previously assumed, however.

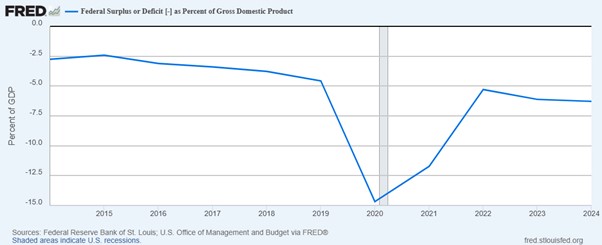

But to the extent the US economy has been growing, this is largely due to the government running a large deficit of 6% of national income.

Total growth last year is estimated at 2.8%. So, the US government added over twice as much debt as the economy generated in growth.

Does that sound sustainable to you? If perhaps that 6% deficit spending was being used for investment it the future, it might be.

But it’s not. In fact, US investment, net of depreciation, has slumped over the past year and now lies at zero.

So, the US has added 6% to the national debt stock in exchange for “growth” of 2.8% and investment in the future at 0%.

I place growth in quotes above because, as you can now see, that 6% deficit was really just funding consumption.

So I ask again: does that sound sustainable to you?

Of course not.

I’m hardly alone. Department of Government Efficiency (DOGE) head, Elon Musk, has commented on X that he finds the spiralling US debt “terrifying”.

DOGE’s mission, with Trump’s blessing, is to try and get that excessive spending under control.

Let’s connect some dots here. The US economy, while weaker than previously estimated, has nevertheless been carrying the rest of the world. Yet it has done so by running up debt to support imports and consumption.

Now, those in charge of the US government want to get that excessive spending under control.

So, guess what happens next: global recession.

But are global stock markets priced for that possibility? Not remotely.

The US, the world’s largest stock market by a wide margin, is priced for perfection, not recession. The price-to-earnings (P/E) ratio on the S&P 500 index is nearly 30, roughly double the long-term historical average.

If that corrects lower, even modestly, it will likely drag global stock market valuations down with it.

This presents investors with a dilemma. Although lower than a year ago, inflation remains positive. It’s been creeping higher again in the US for several months. That trend reversal may soon cross the pond.

Investors need to stay ahead of inflation while also avoiding overvalued stocks.

The solution? Focus on under- or fairly-valued companies instead. There are, in fact, plenty from which to choose.

No, these are not the trendy ones with jet-setting celebrity CEOs giving TED talks or hobnobbing with Hollywood or other glitterati. In some cases, they’re probably companies you’ve never heard of.

They don’t promise a better future full of wonder-widgets. But they do keep the lights on. The motors running. They fill your kitchen cabinets and fridge and empty your bins. They provide essential services of all sorts.

Perhaps that sounds boring. But boring helps to explain why many traditional, bread-and-butter industries are not trading at particularly high valuations at present.

They’re out of the limelight. But backstage, they’re generating cash and paying dividends for their investors.

Cash generation and dividends, by the way, tend to keep up with inflation.

Seven FTSE 100 companies currently pay dividends in excess of 8%. A defensive investor could do worse than to have at least a small allocation to one or more of them.

If you’re looking for more actionable and specific advice on where to begin with your portfolio then simply head over here. I explain more about my own personal system, which I’ve been using for my family for 20 years, and how you can join me.

Until next time,

John Butler

Investment Director, Fortune & Freedom