Just a quick note before we get started. As you may have noticed, we’re coming to you today as Investor’s Daily. As we explained on Tuesday, Fortune & Freedom will be coming to you under this new name from today onwards. Please be assured you’ll still get all the same great content as usual and you don’t need to take any action. But please catch up on that announcement here if you missed it.

***

In today’s issue:

- So-called carry trades can drive markets

- But they can also lead to sharp reversals

- Last August was an example. Is another reversal brewing?

For decades, global financial markets have been driven in part by so-called carry trades, or convergence trades. Both share the common characteristic of sourcing cheap funding, wherever to be found, in order to purchase a higher yielding asset.

It’s a form of arbitrage, albeit one not without its risks. A sudden reversal in European convergence trades in 1998 led to the failure of prominent hedge-fund Long-Term Capital Management. Just last August, a surprise rate hike by the Bank of Japan (BoJ) triggered the so-called “mini crash” that saw many tech stocks drop by double-digits in a single day.

How, exactly, does a BoJ rate hike trigger a crash?

Well, if yen interest rates lie below those of other major countries, then traders seeking cheap funding will borrow in yen to fund positions in higher-yielding assets elsewhere. These could include those where the expected returns are high, such as US “Big Tech”.

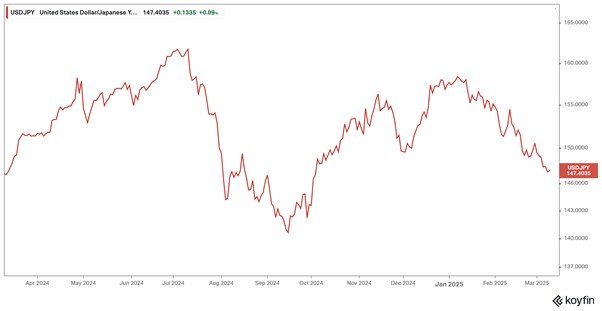

This was the case going into the flash crash. The BoJ raised rates and the yen spiked higher, strengthening from over 160 per US dollar to nearly 140 in just a matter of days. That caused big losses for those traders short the yen. Some were forced to liquidate positions as a result of margin calls. They were carried out, as it were, if not on stretchers.

Source: Koyfin

Source: Koyfin

A few months later, Trump was elected president and the markets recovered. Attention turned elsewhere.

But notice what you also see in the chart above: the yen has been strengthening again, quite possibly in anticipation of more BoJ rate hikes.

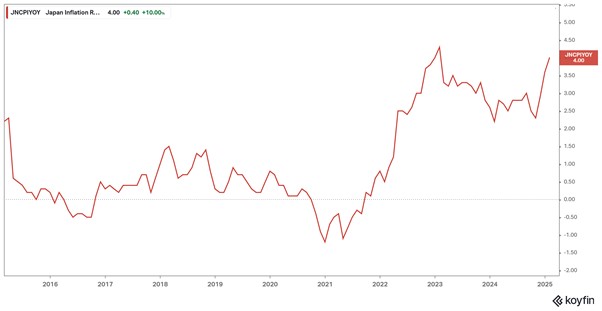

Why would the BoJ hike rates? The global economy is weak and perhaps sliding into outright recession.

But in Japan, inflation has been rising, now up to its highest level for many years. (There was a brief spike in 2023 that was a temporary base effect related to the ending of global Covid lockdowns.)

Source: Koyfin

Source: Koyfin

There is thus good reason for the yen to be stronger. And good reason for traders to be nervous.

If the BoJ raises rates and the yen continues strengthening, something along the lines of August last year could unfold again. It might not be as sudden and dramatic but it would weigh on markets, nonetheless.

Could such concern be contributing to poor stock market performance of late? Absolutely. Add it to the list.

The fact is, at present there are many reasons for caution. As mentioned yesterday, low crude oil and iron ore prices are indications of weak global demand. There are others, including weaking US economic data.

Tariff and trade war concerns are mounting, and their potential impact is nearly impossible to predict. With today’s intricate global supply chains and value-added networks, even experts struggle to model the full extent of the damage. Multinational corporations probably can’t even precisely model the impact on their own businesses.

Yet notwithstanding recent weakness, stock market valuations remain historically elevated, especially in the US. But that’s due largely to the extremely high multiples placed on a small number of companies, including the Magnificent Seven tech firms.

Never in history have such a small number of firms so dominated global stock markets, especially those reliant primarily on “intangibles”, such as brand value or intellectual property, for their lofty valuations.

There is a saying that bull markets always climb a wall of worry. I agree. But once you’ve climbed that wall to historically high valuation multiples, seemingly small things can have a disproportionate impact on prices.

Merely a return to a modest, sub-20 price-to-earnings (P/E) ratio for the S&P 500 would send prices down by 1/3. Again, most of that might be due to a sharp correction in the Big Tech sector. But it is hard to imagine the broader market escaping with less than a double-digit percentage decline.

It could be far worse than that. Last month I wrote about how rising tariff and trade war fears were likely the proximate cause for the October 1929 US stock market crash, one that would eventually wipe out some 90% of market value.

That’s not a prediction, merely an observation. But were it to occur, it would be yet another example of history not exactly repeating but certainly rhyming.

Until next time,

John Butler

Investment Director, Investor’s Daily

Now or Never

Bill Bonner, writing from Baltimore, Maryland

We’re talking about betrayals.

Disappointment.

Faithlessness.

Markets Insider:

Another red day on Wall Street: Trump’s latest tariff threats bring the market-cap wipeout to $5 trillion.

How do investors feel? They expected a big boom. They thought they’d get rich.

Disappointment seems to be spreading. Polls of CEOs and consumers show deepening pessimism. AP:

Inflation, looming trade war take a toll as confidence of the U.S. consumer tumbles

They were looking for a Golden Age… but the gold seems to be turning into base metal.

Tuesday brought more leaden news. CNN:

President Donald Trump backed down from an extraordinary trade war escalation Tuesday that had threatened a massive surge in tariffs on Canadian steel and aluminum and new tariffs on Canadian electricity. In turn, Ontario paused surcharges on electricity to US customers. After the back-and-forth tariff threats that sent markets sharply lower for a second day Tuesday, US Commerce Secretary Howard Lutnick, Canada’s Minister of Finance Dominic LeBlanc and Ontario Premier Doug Ford said they would meet Thursday to renegotiate the free trade treaty known as the USMCA.

What are Canadians supposed to think? Will this next round of talks settle the issue? Maybe. But once betrayed, they may be skeptical that they can trust the giant to their south.

The Trump team is making a big mistake, says Charles C.W. Cooke at National Review. Trump spends his time and attention on distractions that don’t matter to the people who elected him.

Greenland, Canada as 51st state, the Panama Canal, Trump Gaza, bad-mouthing reporters, opinion writers and opposing politicians – with so much fur flying, it is easy to lose sight of the real promise of Trump’s win. Mediate:

President Donald Trump “is at risk of blowing his second term before it has hit the two-month mark,” wrote National Review senior editor Charles C. W. Cooke to kick off his latest column about the president’s hectic last few weeks, criticizing him for getting distracted by “stupid, irrelevant indulgences” instead of the core issues that led voters to re-elect him.

One of those ‘stupid, irrelevant indulgences’ is Trump’s attack on Thomas Massie. He believes Massie has betrayed the MAGA cause. Almost alone among the yes monkeys in Congress, Massie sticks to the core issues. He wonders how any Republican can vote to continue spending money on wasteful and unnecessary programs – including those revealed by Trump’s own DOGE task force.

But that’s the charm of betrayal… it can work in both directions.

Massie believes it is he who has been betrayed. He thought the MAGA folks were going to drain the swamp. But there it was in front of him…a Continuing Resolution with more than 1,500 pages of boondoggles… bamboozles… and BS. USA Today:

“Unless I get a lobotomy Monday that causes me to forget what I’ve witnessed the past 12 years,” Massie said in a post on X Sunday, “I’ll be a NO on the CR this week.”

“Why would I vote to continue the waste, fraud and abuse DOGE has found,” the Kentucky representative wrote.

The big, beautiful bill also increases the debt level by $2 trillion per year over the next two years – bringing it over $40 trillion before the next mid-terms. It adds $3 trillion to deficits already programmed in the system. And it pulls the rug on Musk and his band of Jacobin cost cutters.

Why keep funding waste, they might ask?

And Mr. Trump, why not just tell Congress to come up with a balanced budget…or he won’t sign?

Imagine the approval he would get – at least from us! – if he were to announce: “Debt is out of control. I’m drawing the line right here, right now.”

He might even recycle the momentous line of Malcolm X, “If not us, who… If not now, when?”

As it is, the CR merely continues the spending pattern of the last 25 years. No wonder people feel let down.

Stay tuned.

Regards,

Bill Bonner

Contributing Editor, Investor’s Daily

For more from Bill Bonner, visit www.bonnerprivateresearch.com