Yesterday, I traced the straight line from the 1916 Sykes-Picot agreement, through a century of oil-driven conflict, to the bombs falling on Iran right now.

Yesterday, I traced the straight line from the 1916 Sykes-Picot agreement, through a century of oil-driven conflict, to the bombs falling on Iran right now.

Or at least I tried to condense what is an incredibly complex geopolitical history into something relatively direct and easy to follow.

The point being that oil is really the name of the game in this conflict. But that should surprise no one.

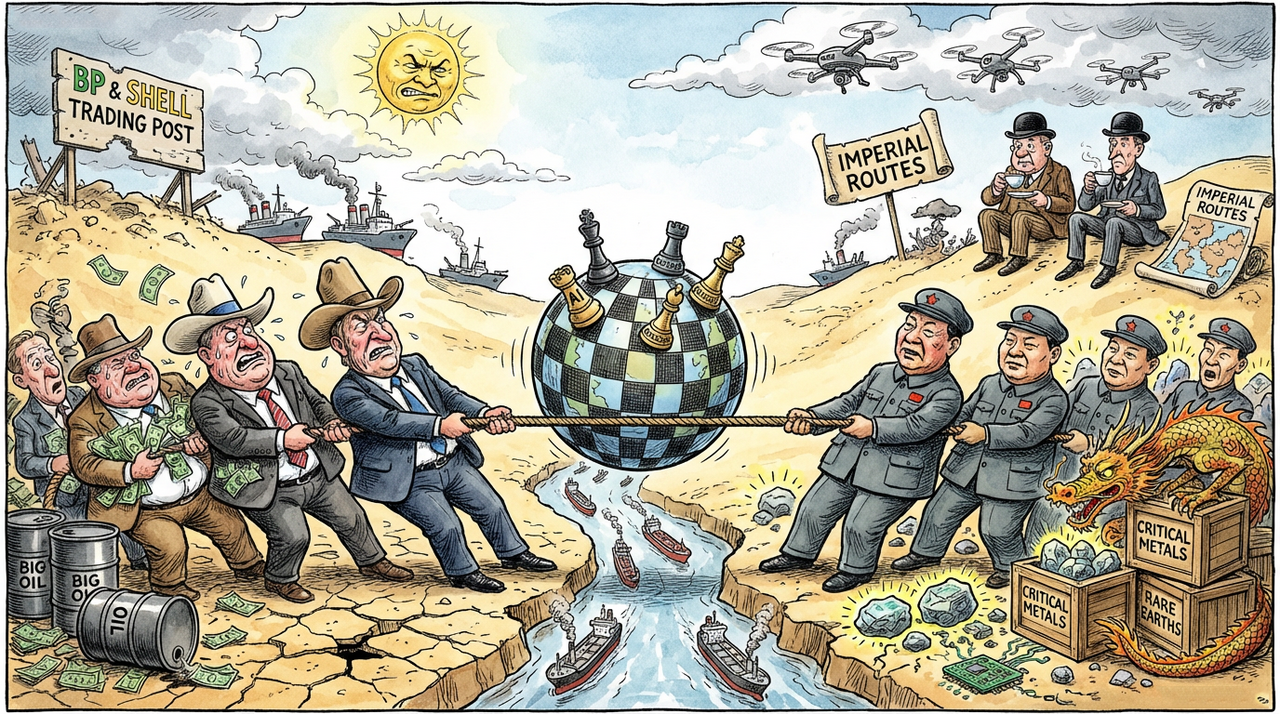

BP [LON:BP] became a strategic powerhouse out of the Sykes-Picot era. British Petroleum literally began as the Anglo-Persian Oil Company, Churchill’s strategic play to fuel the Royal Navy. Shell’s [LON:SHEL] roots in the Middle East run just as deep after being a primary beneficiary of the carve up of the Ottoman Empire.

But in 2026, these companies are no longer the primary beneficiaries of Middle Eastern conflict.

They still produce and refine oil globally, and higher crude prices lift their earnings. BP is yielding over 5% right now and remains a solid dividend play. But neither BP nor Shell is positioned to capture the most asymmetric gains from this particular disruption.

The real winners sit across the Atlantic.

Shutting off supply

ExxonMobil [NYSE:XOM] is trading near its all-time high, around US$150 and is already up roughly 23% year to date. The company produced 4.7 million barrels of oil equivalent per day last quarter, beat earnings estimates and committed to US$20 billion in share buybacks for 2026.

Chevron [NYSE:CVX] hit a new 52-week high in the early days of the conflict, trading well over US$190. Its breakeven level for maintaining spending and dividends sits around US$50 a barrel, which means that at current prices the company is generating enormous free cash flow.

These are companies built for exactly this kind of environment.

ConocoPhillips [NYSE:COP], Marathon Petroleum [NYSE:MPC], and Diamondback Energy [NASDAQ:FANG] are all in the same boat.

Hence it’s no surprise that the energy sector has been the top-performing S&P 500 sector in 2026, up nearly 27% year-to-date while technology stocks have slipped into the red. That rotation was already underway before Iran. The war has now accelerated it.

Now, I still believe this conflict is largely about oil. And I say that partly because of the action the US has taken in Venezuela as well.

But if you’re thinking perhaps there’s even more to this than deep historic control of oil, you might also be right…

Qatar produces roughly 20% of the world’s liquefied natural gas. When Iran struck Qatar’s Ras Laffan facility and effectively blocked the Strait of Hormuz, that entire supply went offline overnight. Qatar declared force majeure on exports.

If you like a good mystery, then consider this. The US likely knew exactly how Iran would respond. And the real strategic move here may not simply be about controlling Middle Eastern supply. It may also be about squeezing China.

China gets about 38% of its crude oil through the Strait of Hormuz.

When that chokepoint closed, it didn’t just disrupt Qatari LNG. It threatened the energy lifeline that keeps the world’s second-largest economy running.

China has a strategic petroleum reserve, but estimates vary wildly on how long it lasts — anywhere from 40 to 90 days.

If the Strait remains contested, and the US is not especially motivated to reopen it quickly (despite public claims), China could face an energy shock that Washington might actually welcome.

And that creates a very specific kind of leverage.

It’s critical to these metals

China also happens to control the global supply of several critical metals that sit at the heart of the AI, semiconductor and defence build-outs every Western nation is racing to complete.

We’re talking about antimony, gallium, germanium.

Materials most people have never heard of, but without which modern chips, infrared optics, military-grade electronics and solar panels cannot be produced.

There is a good reason these metals were all designated strategically important to US national security by President Trump.

China refines around 80% of the world’s gallium and germanium. It also controls a dominant share of global antimony supply. Beijing has already weaponised that position, restricting gallium and germanium exports since mid-2023 and tightening antimony controls in late 2024.

Here’s where it gets interesting.

If the US and its allies are effectively squeezing China’s energy imports by keeping the Strait contested, China’s leverage over critical metals becomes a bargaining chip, not a trump card. It is difficult to pressure the US with mineral supply restrictions while your own energy lifeline is being threatened.

Whether this is by design or accident is the conspiracy question.

But the result is the same.

The conflict is exposing a codependency that both sides have been dancing around for years. China needs energy routes that run through waters it doesn’t control. Meanwhile, the West relies on refined metals from supply chains it does not own.

Feels a bit like a good old fashioned Mexican standoff.

The US and its allies are painfully short of domestic refining capacity for these metals. That was a known vulnerability before the first missile was launched. Now it’s front and centre.

The nations and companies that can build or secure alternative supply chains for antimony, gallium and germanium will hold a major advantage in the AI and defence arms race that shows no sign of slowing down.

Which makes investing in critical metals, commodities and resource production arguably one of the most important opportunities of 2026.

Of course, the risks are real.

If the conflict resolves quickly and the Strait reopens, the pressure on China’s energy supply eases immediately. A rapid de-escalation would likely take the geopolitical premium from markets almost as quickly as it appeared.

But even if this war ended tomorrow, the world has just received a brutal reminder.

Critical mineral supply chains and energy corridors had been operating as though geopolitical risk barely existed.

That illusion has now been shattered.

The race to secure domestic sources and strategic reserves of oil, gas and the metals underpinning next-generation military, AI and semiconductor infrastructure has suddenly become the highest priority for governments everywhere.

A century ago, Churchill needed oil and reached into the Middle East to get it.

They are oil — plus the antimony in flame retardants, the gallium in radar systems, the germanium in fibre optics and the advanced AI hardware – capable of guiding a drone to a target the size of a football from 10,000 miles away.

The Sykes-Picot era created oil giants in BP, Shell, and Chevron. This era will create a new generation of critical resource giants.

Which companies those will be…

Only time will tell.

Regards,

Sam Volkering

Investment Director, Southbank Investment Research