In today’s Issue:

In today’s Issue:

- What’s the next big idea?

- We live under the tyranny of Monetary Dominance

- There is only one way out

Big ideas are nasty things, especially in the heads of politicians. It’s bad enough when leaders are just self-serving narcissists. Give them a whiff of self-righteousness fuelled by ideology, and things go completely off the rails.

The infamous John Maynard Keynes knew his ideas would cause chaos. He even said so in the book that laid them out:

“The ideas of economists and political philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed, the world is ruled by little else.

“Practical men who believe themselves to be quite exempt from any intellectual influence are usually the slaves of some defunct economist.

“Madmen in authority, who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back.”

Keynes was right. About this, anyway.

Those who experienced socialism and communism know all about it firsthand.

But lately, the academic scribblers have been working overtime. We’ve had all sorts of ideologies come and go in recent years. Not to mention the many madmen in authority who listened to the voices in their think tank.

Before 2008, it was the Monetarists in charge. They couldn’t see the epic housing bubble they inflated. Because it didn’t show up in consumer price inflation data.

Then we had the Keynesianism of fiscal stimulus after 2008. The monetarist economist Milton Friedman is famous for pointing out that “we are all Keynesians” in a crisis.

Austerity took a brief turn at the helm around 2010 in Europe. Nobody owns up to that one now.

In 2020, we got another crisis and its Keynesian response.

In 2021, Modern Monetary Theory took over. That didn’t last very long!

Neither did 2022’s “grow your way out of debt” strategy in the UK.

Most of these ideologies ended up being proven wrong. Indeed, they have an odd habit of creating precisely the opposite outcome to the one intended. I think it’ll be quite some time before anyone tries MMT again!

Economists call the disastrous fallout of their policies “unintended consequences.” It’s their a “get out of jail free card.” In some cases, literally.

It’s interesting that ideologies that are so wrong can still have such a big impact.

But why dwell on the past? Because the latest grand theory we are all slaves to is here…

We are all Fiscal Dominance now

The latest ideology to take hold in the heads of madmen in authority is called “Fiscal Dominance”. In coming months, everyone will think they know what it means. Heck, the idea will become so fashionable that people will just adjust the theory to fit the facts.

But here are the basics…

There are supposed to be two policy tools to keep the economy chugging along. Fiscal policy from the government in the form of taxes and spending. And monetary policy from the central bank in the form of interest rates and the money supply.

For centuries, economists have argued about who should do the heavy lifting and how.

But in 2020, something fundamental changed. So say the theories of Fiscal Dominance, anyway.

Because of COVID spending, governments are now overindebted. This means central bankers have lost control of monetary policy. They cannot raise interest rates without making the government go broke.

And so monetary policy is dead in the water. Central bankers are too busy trying to keep the government afloat to worry about inflation.

That leaves fiscal policy as the dominant power in economic policy. Which means the Treasury is now in the driver’s seat. It must steer the economy towards growth but away from inflation.

All of this is, of course, a complete load of rubbish…

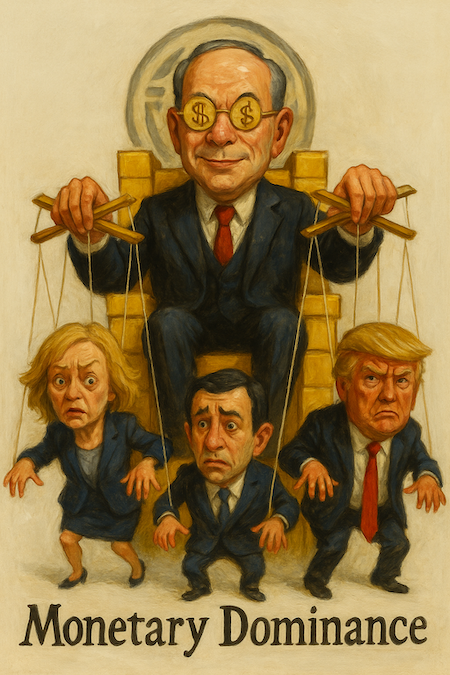

Fiscal Dominance has it precisely backwards

Central banks control governments. We live under a system of Monetary Dominance, not fiscal.

It’s obvious…

Did Liz Truss fire the Bank of England, or did the Bank of England get rid of her?

Did Greek PM Alexis Tsipras fiscally dominate European Central Bank president Christine Lagarde? Or did she force him to ignore a referendum result against austerity?

Did Matteo Salvini call the ECB to heel after declaring the euro a “crime against humanity”? Or did he install a former ECB president as Prime Minister?

Did Trump manage to fire Jerome Powell? Or did he have to delay his tariff policies when the bond market cracked under Powell’s excessively tight monetary policy?

Did Ben Bernanke save the financial system, or President Bush? (I had to look up who was president in 2008, which answers the question rather well.)

The world trembled each time Bank of Japan governor Kuroda laughed like a maniac because of his poor English. Nobody ever bothered to look for Shinzo Abe’s three arrows after they missed the target.

If you think politicians are the ones in control, you’re blind.

Revolving door at the printing press

Admittedly, it’s all too often the same people in charge.

Lagarde was the French Finance Minister before leading the IMF and then the ECB.

Before he was Treasury Secretary, Tim Geithner was New York Fed Chair, where he actually implemented the Fed’s monetary policy. Heck, Tim got stuck in the revolving door. Before his time at the Fed, he was at the Treasury.

Fed chair Yellen became Treasury Secretary.

Current Treasury Secretary Bessent is the odds on favourite for next Fed Chair.

The Bank of England’s Mark Carney came from the Bank of Canada and recently became the Prime Minister of Canada.

ECB President Draghi became PM of Italy.

And the list goes on and on and on. So, perhaps the monetary and fiscal authorities are a bit of a blur at this point.

The choice between democracy and bond yields

It’s crystal clear to me that governments are powerless. They rely on their central bank to keep the bond market ticking over.

The promise of imminent QE should anything go wrong cannot be put at risk. Governments can only do what their central bank will rubber stamp. Or else…

Italian politician Claudio Borghi explained the general situation most eloquently back when he discovered all this the hard way during the European Sovereign Debt Crisis:

In a way, I am very happy because we have finally wiped the bull**** off the table. We now know that it is a choice between democracy or comfortable bond spreads. You have to swear allegiance to the god of the euro in order to be allowed to have a political life in Italy. It’s worse than a religion.

What we are seeing is the fundamental problem with the eurozone construction; You can’t have a government that displeases the markets or the spread club. The ECB and the Eurogroup will use this to crush your economy. You are very lucky in the United Kingdom that you still live in a free country.

Not anymore. Not since our own debts crept over the invisible line that makes us reliant on the Bank of England’s imminent bailout should the bond market tank.

And so we have central bankers giving their “opinions” about things like Brexit and taxes. These are not-so-subtle hints that the government is one step away from losing the Bank of England’s support in the bond market. Or should I say threats?

Of course, the Bank claims it isn’t interfering in politics. But you can’t claim to be politically independent and then back your horse with an unlimited budget of QE while selling the bonds of your detractors the day before their budget!

But the central bank is doing just that.

So Fiscal Dominance has it wrong. Central bankers are the dominant ones. Not treasuries.

The key debate in British politics today isn’t about bond markets, voters, quangos, elections, taxes, spending cuts or political promises. It’s a simple question: what economic policy will the Bank of England support in the bond market? And what will cause it to delay that support for long enough to let the bond market stumble, forcing any politician to reverse course? Or resign…

There is only one way for a government to fix all this. It needs to trigger vast economic growth by boosting productivity and raise more tax revenue at the same time.

And there is only one way to do that right now.

Until next time,

![]()

Nick Hubble

Editor, Investor’s Daily

P.S. I’ve read the history books—and I’ve seen what happens when a rush like this begins. But this time, it’s not gold nuggets panned from rivers… it’s a $150 trillion treasure trove of rare earths finally unlocked by Trump’s Supreme Court. Jim Rickards believes this could be the biggest wealth wave of our lifetime—and after hearing his breakdown, I think he might be right. Here’s where it starts.